Hi! it’s Laura from Nanny Parent Connection, back with this week’s video.

Let’s tackle a question we have heard more and more recently: do nannies need to purchase any type of insurance?

There is a lot of confusion out there on this topic. Today, we’ll explore the ins and outs of insurance for nannies, focusing on what types of coverage are essential and what might be optional extras.

(This video will not discuss the types of insurance that families should consider purchasing if they employ a nanny. To learn more about that, please watch this video.)

Click the button below to watch and we hope you find this video helpful!

If you found this video helpful, please subscribe on YouTube and share it with your friends. Also, please take a moment to check out the other videos we have published on YouTube.

We’d love to hear any comments about how we can improve these videos as well as your ideas on topics you’d like to see us cover in the future. Just comment below!

If you aren’t currently a member of our community, we’d love to have you join. Nannies and sitters can join our community totally FREE and our Family/Parent memberships start at only $8.99/month!

Don’t forget, you can reach us directly via email by clicking here or by calling/texting (425) 243-7032 if we can help you.

A transcript of the video can be found below:

Hi, it’s Casey from Nanny Parent Connection back with this week’s video.

Let’s tackle a question we have heard more and more recently: do nannies need to purchase any type of insurance?

Today, we’ll explore the ins and outs of insurance for nannies, focusing on what types of coverage are essential and what might be optional extras.

This video will not discuss the types of insurance that families should consider purchasing if they employ a nanny. For information on that, click here.

Let’s start with the basics

Generally, nannies don’t need to worry about purchasing any types of insurance products, except for auto insurance.

If you’re using your personal vehicle to transport the children you care for, auto insurance becomes essential.

It ensures you and your nanny kids are protected in case of any accidents while on the job.

Here’s the catch: your personal auto insurance may not cover you if you’re using your car for work-related tasks.

In such cases, your insurance provider might require you to switch to a commercial auto policy, which can be notably more expensive.

However, there are options to explore, such as obtaining business class rates on your existing personal policy.

Contact your auto insurance agent or company to explore what options they can offer you. Make sure you have adequate coverage for transporting children.

Many Insurance professionals recommend bodily injury limits of at least $100,000 per person and $300,000 per accident, at a minimum.

For the vast majority of nannies, auto insurance is the only insurance product that you need to worry about, and that is only if you’re using your personal vehicle to transport nanny kids.

If nannies want to go above and beyond to ensure they are covered in case of any event or circumstance, they can purchase personal liability insurance or personal injury coverage.

First up, let’s discuss personal liability insurance

This coverage protects you in case you accidentally cause harm or damage while working. Imagine a scenario where you’re playing with the children and accidentally break something valuable, like an expensive vase or electronics equipment, or when playing with your nanny child, you accidentally injure them.

Personal liability insurance can cover the costs, ensuring both you and the family you work for are protected.

Specifically, it will cover medical expenses, property damage, and legal fees in case of a lawsuit. Insurance professionals recommend having sufficient coverage with liability limits of at least $1,000,000 dollars.

This ensures adequate protection against potential liabilities.

While it is easy to add personal liability insurance coverage to your home, condo, or renters insurance policy, watch out: these types of insurance policies can be very expensive.

Make sure to shop around if you decide to purchase one of these policies.

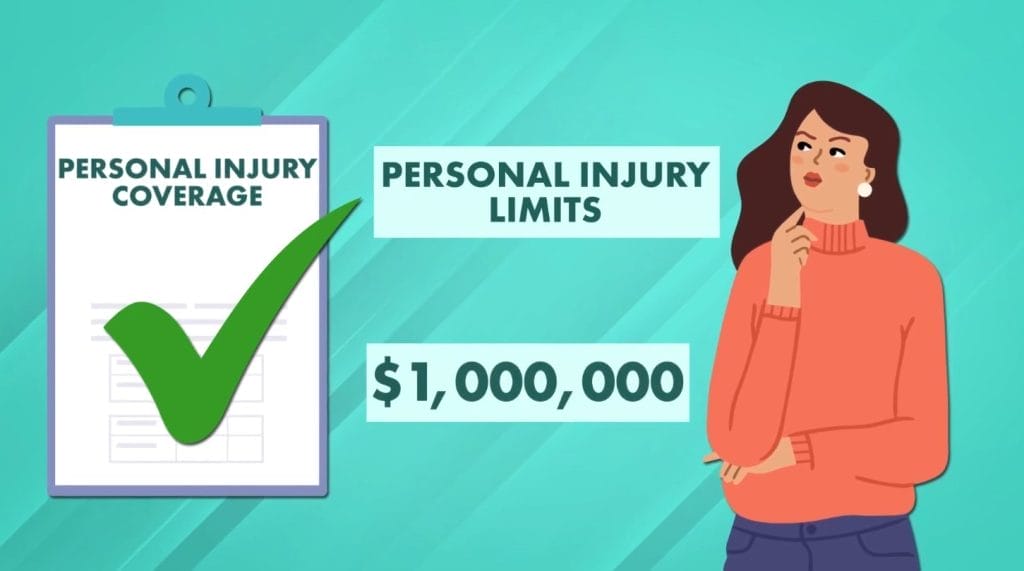

Additionally, personal injury coverage is worth considering

Personal injury coverage protects you from defamation lawsuits and claims of libel, slander, or defamation.

In today’s litigious society, this coverage provides essential protection against potential legal disputes arising from your interactions while working.

What if you were to say something at a play date that someone else misheard or claimed was inappropriate?

Having this coverage could protect you and your nanny family if sued. Personal injury coverage extends to incidents such as miscommunication or misunderstandings that could lead to defamation claims.

It ensures you’re financially covered in case someone alleges that your actions or words have caused harm to their reputation.

Unlike personal liability insurance, personal injury coverage is often surprisingly affordable to add to your existing home, renters, or condo insurance policy.

Considering its relatively low cost compared to its potential benefits, it can be a worthwhile investment for nannies.

If you do decide to set up personal injury coverage, insurance professionals recommend personal injury limits of at least $1,000,000 dollars.

This ensures comprehensive protection against potential defamation lawsuits and associated legal expenses.

Now you might be wondering, do parents expect nannies to have their own personal liability insurance or injury coverage? The vast majority don’t.

While our team has only worked with a small handful of nannies that carry either personal liability insurance or personal injury coverage, we have noticed an uptick in nannies in our community exploring insurance coverage products, demonstrating an increased awareness of the importance of protection.

So, do nannies need to purchase their own insurance?

In short, auto insurance is a must if you’re transporting children for your job, and if you want that extra layer of protection, consider personal liability or injury coverage.

It’s all about ensuring you’re prepared for whatever comes your way.

We hope you found this information useful, and if you want to learn more about insurance in the nanny world, check out this video: “Do You Need To Add Your Nanny To Your Car Insurance?”

Thanks for watching, and don’t forget to like, subscribe, and share this video.

Talk with you next week!